Download presentation

Presentation is loading. Please wait.

1

Understanding of Economic Principles 2016. 10. 4 서병한

2

What is Economics ? Is economics about money: How people make it and spend it? I s it about business, government, and jobs? Is economics about why some people and some nations are ric h and others poor? Economics is about all these things, but its core is the study of choices and their consequences. Your life will be shaped by the challenges you face and the opportunities that you create. But to face those challenges and seize the opportunities, you must understand the powerful forces at play. The economics that you’re about to learn will become your most reliable guide.

3

Demand and Supply Goal of Life: 행복 ( 욕구 ) ∞, the more the better Means of Satisfaction: resources and income, finite → The Law of Scarcity, Budget Constraint HH max U(X 1, X 2 ) s.t P 1 X 1 + P 2 X 2 ≤ Money → the Law of Deamnd

∞, the more the better Means of Satisfaction: resources and income, finite → The Law of Scarcity, Budget Constraint HH max U(X 1, X 2 ) s.t P 1 X 1 + P 2 X 2 ≤ Money → the Law of Deamnd")

4

The Law of Demand

5

The Law of Supply Firms max PX – (WL + rK) → the Law of Supply

→ the Law of Supply")

6

Market Equilibrium: Predicting Changes in Price and Quantity

7

Market vs Government: 시장이 실 패하면 정부가 개입해야 하는가 ? 완전경쟁시장은 희소한 자원을 가장 효율적으로 배분함으로써 국민후생을 증진시킨다 (Adam Smith, 1776) Mkt Failure: Monopoly, External (dis)Economy- 환경오염, Public Goods, etc Gov’t Failure: Iron Triangle - Public Choice Theory(Relationship Capitalism; 천민적 자본 주의 ), Distortion of Incentives,

Mkt Failure: Monopoly, External (dis)Economy- 환경오염, Public Goods, etc Gov’t Failure: Iron Triangle - Public Choice Theory(Relationship Capitalism; 천민적 자본 주의 ), Distortion of Incentives,.")

8

Economic System 3 Basic Economic Problems: What, How, For Whom to produce How to solve 3 Basic Economic Problems 1. Market Economy 2. Central Planning Board 3. Mixed Economy ( 수정자본주의 )

.")

9

Structure of Economy: Financial Flows & Circular Flow of Expenditure and Income

10

Economic Agent: Household, Firm, Gov’t, Foreign Country Economic Object: Goods and Service, Labor, Capital, Asset, Foreign Currency Market: Goods Mkt, Factor(Labor) Mkt, Financial Mkt (Domestic, Foreign Exchange)

Mkt, Financial Mkt (Domestic, Foreign Exchange)")

11

GDP( 국민총생산 또는 국민소득 ) 3 면 등가의 원칙 Y=C + I + G + X 지출측면 Y=C + S + T + M Y= 임금소득 ( 근로자 ) + 자본소득 ( 자본가 ) + 이윤 ( 경영자 ) 분배측면 Y=1 차산업 산출액 + 2 차산업 산출액 + 3 차산업 산출액 산출측면 GDP Identity (X-M) = (S-I) + (T-G)

3 면 등가의 원칙 Y=C + I + G + X 지출측면 Y=C + S + T + M Y= 임금소득 ( 근로자 ) + 자본소득 ( 자본가 ) + 이윤 ( 경영자 ) 분배측면 Y=1 차산업 산출액 + 2 차산업 산출액 + 3 차산업 산출액 산출측면 GDP Identity (X-M) = (S-I) + (T-G)")

12

Financial Statements: Balance Sheet & Profit and Loss Sheet Balance Sheet(B/S) records assets and liabilities at a particular time. ㅇㅇ 대 차 대 조 표 ㅇ년 ㅇ월 ㅇ일 현재 자 산 부 채 현금 예금 ㅇㅇ차입금 ㅇㅇ 기계, 공장 ㅇㅇ채권 ㅇㅇ... 자산합계 ㅇㅇ 부채합계 ㅇㅇ

13

B/S of Each Economic Agen Consider Bank’s B/S Consider Bank’s B/S Consider Central Bank’s B/S Consider Government’s B/S Consider Your’s B/S

14

Profit and Loss Sheet records profits and losses over a period of time. Human Capital ( 인적자본 ): 창의 ( 조 ) 성으로 수익 을 창출하는 능력 Consider Life-Cycle Hypothesis(LCH) of Consumption: dissaving when young and old is covered by saving when working. 자산 = 저축 (y-c=s) 이 축적된 것

: 창의 ( 조 ) 성으로 수익 을 창출하는 능력 Consider Life-Cycle Hypothesis(LCH) of Consumption: dissaving when young and old is covered by saving when working. 자산 = 저축 (y-c=s) 이 축적된 것.")

15

Determination of Asset Price V=E t ∑β j (R t+j ) β j : 할인인자 (factor of discount rate) β : 1/(1+ i t ), i t =1+ r t, r E t (R t+j )=E t [R t+j l Ω t ] : 미래 t+j 시점에서의 수익 R t+j 를 현재 t 에서의 시점 정보집합 Ω t 를 이용하 여 합리적으로 예상한 합리적 기대 (Rational Expetations) 따라서 자산가격은 자산으로부터 예상되는 미래 수익흐름의 현재할인가치 (discounted value of future expected revenue) 에 의해 결정된다.

![Determination of Asset Price V=E t ∑β j (R t+j ) β j : 할인인자 (factor of discount rate) β : 1/(1+ i t ), i t =1+ r t, r E t (R t+j )=E t [R t+j l Ω t ] : 미래 t+j 시점에서의 수익 R t+j 를 현재 t 에서의 시점 정보집합 Ω t 를 이용하 여 합리적으로 예상한 합리적 기대 (Rational Expetations) 따라서 자산가격은 자산으로부터 예상되는 미래 수익흐름의 현재할인가치 (discounted value of future expected revenue) 에 의해 결정된다.](http://images.slidesplayer.org/47/11710250/slides/slide_15.jpg "Determination of Asset Price V=E t ∑β j (R t+j ) β j : 할인인자 (factor of discount rate) β : 1/(1+ i t ), i t =1+ r t, r E t (R t+j )=E t [R t+j l Ω t ] : 미래 t+j 시점에서의 수익 R t+j 를 현재 t 에서의 시점 정보집합 Ω t 를 이용하 여 합리적으로 예상한 합리적 기대 (Rational Expetations) 따라서 자산가격은 자산으로부터 예상되는 미래 수익흐름의 현재할인가치 (discounted value of future expected revenue) 에 의해 결정된다.")

16

자산을 사거나 팔 경우 미래 예상수익이 불 확실하므로 불확실성 하에서 의사결정을 해야 한다. Bond 수익 : 이자소득 (Interest Income) Stock 수익 : 배당금 (Dividend) Human Capital: ?

Stock 수익 : 배당금 (Dividend) Human Capital: .")

17

인플레이션과 실업, 경기변동 Explain the short-run and long-run tradeoff between inflation an d unemployment Explain how the mainstream business cycle theory and real business cycle theory account for fluctuations in output and employment We care about inflation because it raises our cost of living. We care about unemployment because it takes our jobs. We want low inflation, low unemployment, and rapid income growth. But can we have all these things at the same time? Or do we face a tradeoff among them?

18

Short-run Trade-off b/t Inflation and Unemployment

19

AD(Aggregate Demand)=C+I+G+(X-M) AS(Aggregate Supply)=f(wage, i, S, E t Y t+i …) Business Cycle( 경기변동 ) 호황 : 현재 산출 > 자연 산출 → 물가상승, 실업감소 불황 : 현재 산출 < 자연 산출 → 물가하락, 실업증가

=C+I+G+(X-M) AS(Aggregate Supply)=f(wage, i, S, E t Y t+i …) Business Cycle( 경기변동 ) 호황 : 현재 산출 > 자연 산출 → 물가상승, 실업감소 불황 : 현재 산출 < 자연 산출 → 물가하락, 실업증가")

20

총수요 관리정책 Monetary Policy: 불경기에 금리인하 → 소비 및 투자진작 → 단기적으로 소득 및 물가 상승 → 실질 임금 (W/P) 하락 → 노동조합 및 근로자 명목임금 인상요구 → 장기적으로 소득은 자연산출 수준에 서 불변하고 인플레이션만 상승 가계, 기업, 노조 등이 합리적으로 기대를 하면 중 앙은행이 금리인하 → 기대인플레이션 상승 → 곧 바로 명목임금 상승, 제품가격 인상, 인플레이션 및 명목금리 상승 → 산출량 ( 실업 ) 을 불변하고 물 가만 상승 : 정책무력성 (Policy Ineffectiveness)

하락 → 노동조합 및 근로자 명목임금 인상요구 → 장기적으로 소득은 자연산출 수준에 서 불변하고 인플레이션만 상승 가계, 기업, 노조 등이 합리적으로 기대를 하면 중 앙은행이 금리인하 → 기대인플레이션 상승 → 곧 바로 명목임금 상승, 제품가격 인상, 인플레이션 및 명목금리 상승 → 산출량 ( 실업 ) 을 불변하고 물 가만 상승 : 정책무력성 (Policy Ineffectiveness)")

21

정책신뢰성 Policy Credibility : 중앙은행이 금리를 조절할 때 기대 인플레이션이 현재 인플레이션 수 준에서 일정하게 주어져 있다고 가정하는 것은 국민을 바보로 간주하는 것 → 이러한 정부의 단기적인 통화정책은 국민을 속이 는 (fooling people) 꼼수임 : 합리적인 국민은 한 번 속지 계속 반복적으로 속지 않는다. (Example) 어린아이 교육, 특허정책 등

어린아이 교육, 특허정책 등.")

22

足食 足兵 民信 無信不立 - 논어 If policy is incredible, good intentions but bad results will be realized !!

23

The Foreign Exchange Market W + S $ =Y dW/d $ = -(1/S): 명목환율 (nominal S)= 원화와 달러화의 교환 비율 PX + SP*M = Y dX/dM= -(SP*/P): 실질환율 (real S)= 국산품과 수입품의 교환비 율 W: 자국통화 $ : 외국통화 S: 환율 Y: 통화보유액 P: 국내물가 P*: 외국물가 X: 국산 ( 수출 ) 품 M: 수입품 달러에 대한 수요는 수입 (M) 과 자본유출 (KO) 에 의해, 달러공급은 수출 (X) 과 자본유입 (KI) 에 의해 결정된다. KO: 해외투자 ( 미국국채매, 해외공장설립 ), 외국대출 KI: 외국인투자 ( 채권, 주식, 부동산 ), 외국차입

, 외국대출 KI: 외국인투자 ( 채권, 주식, 부동산 ), 외국차입.")

24

Determination of Foreign Exchange Rate

25

Equilibrium in f.e Mkt : (X+KI)=(M+KO) Depreciation: 원화가치 절하 = 달러가치절상 Appreciation: 원화가치 절상 = 달러가치절하 BOP(Balance of Payments)=CA +KA CA(Current Account)=(X-M) KA(Capital Account)=(KI+KO) From GDP Identity, (X-M) = (S-I) + (T-G)

=(M+KO) Depreciation: 원화가치 절하 = 달러가치절상 Appreciation: 원화가치 절상 = 달러가치절하 BOP(Balance of Payments)=CA +KA CA(Current Account)=(X-M) KA(Capital Account)=(KI+KO) From GDP Identity, (X-M) = (S-I) + (T-G)")

26

Exchange Rate Fluctuations Fundamentals, Expectations, and Arbitrage –The exchange rate changes when it is ex pected to change. –But expectations about the exchange rate are driven by deeper forces. –Two such forces are Interest rate parity Purchasing power parity

27

Interest Rate Parity( 금리평가이론 ) –A currency is worth what it can earn. –The return on a currency is the interest rate on that currency plus the expected rate of app reciation over a given period. –When the rates of returns on two currencies are equal, interest rate parity prevails. –Interest rate parity means equal interest rate s when exchange rate changes are taken into account. –Market forces achieve interest rate parity ver y quickly.

28

Purchasing Power Parity( 구매력평가이론 : 일물일가의 법칙 )) –A currency is worth the value of goods and se rvices that it will buy. –The quantity of goods and services that one u nit of a particular currency will buy differs fro m the quantity of goods and services that one unit of another currency will buy. –When two quantities of money can buy the sa me quantity of goods and services, the situati on is called purchasing power parity, which m eans equal value of money.

29

Instant Exchange Rate Response –The exchange rate responds instantly to news about changes in the variables that influence demand and supply in the foreign exchange market. –Suppose that Federal Reserve Bank(Fed) is considering raising the interest rate next week. –With this news, currency traders expect to the demand for Dollar to increase and the demand for Wo ns to decrease—they expect the U.S. dollar to appreciate.

is considering raising the interest rate next week. –With this news, currency traders expect to the demand for Dollar to increase and the demand for Wo ns to decrease—they expect the U.S. dollar to appreciate..")

30

But to benefit from a Dollar appreciation, Won must be sold and dollars must be bought before the exchange rate changes. Each trader knows that all the other traders share the same information and have similar expectations. Each trader knows that when people begin to sell Wo n and buy Dollar, the exchange rate will change. To transact before the exchange rate changes means transacting right away, as soon as the news is received.

31

The Real Exchange Rate –The real exchange rate is the relative price of U.S.-produced goods and services to foreign- produced goods and services. –It measures the quantity of real GDP of other countries that a unit of domestic real GDP buys. –The equation that links the nominal exchange ra te (S) and real exchange rate (RER) is RER = (S x P)/P* –where P is the domestic price level and P* is the U.S. price level.

and real exchange rate (RER) is RER = (S x P)/P* –where P is the domestic price level and P* is the U.S. price level..")

32

The Short Run –In the short run, the equation determines RER. RER = (S x P*)/P –In the short run, if the nominal exchange rate changes, P and P* do not change and the change in S brings an equivalent change i n RER.

/P –In the short run, if the nominal exchange rate changes, P and P* do not change and the change in S brings an equivalent change i n RER..")

33

The Long Run –In the long run, RER is determined by the real fo rces of demand and supply in the markets for goo ds and services. –So in the long run, S is determined by RER and the price levels. That is, S = RER x (P/P*) –A decrease in the U.S. price level P* brings a appreciation of the U.S. dollar in the long run. –A rise in the U.S. price level P brings a depreciat ion of the U.S. dollar in the long run.

–A decrease in the U.S. price level P* brings a appreciation of the U.S. dollar in the long run. –A rise in the U.S. price level P brings a depreciat ion of the U.S. dollar in the long run..")

34

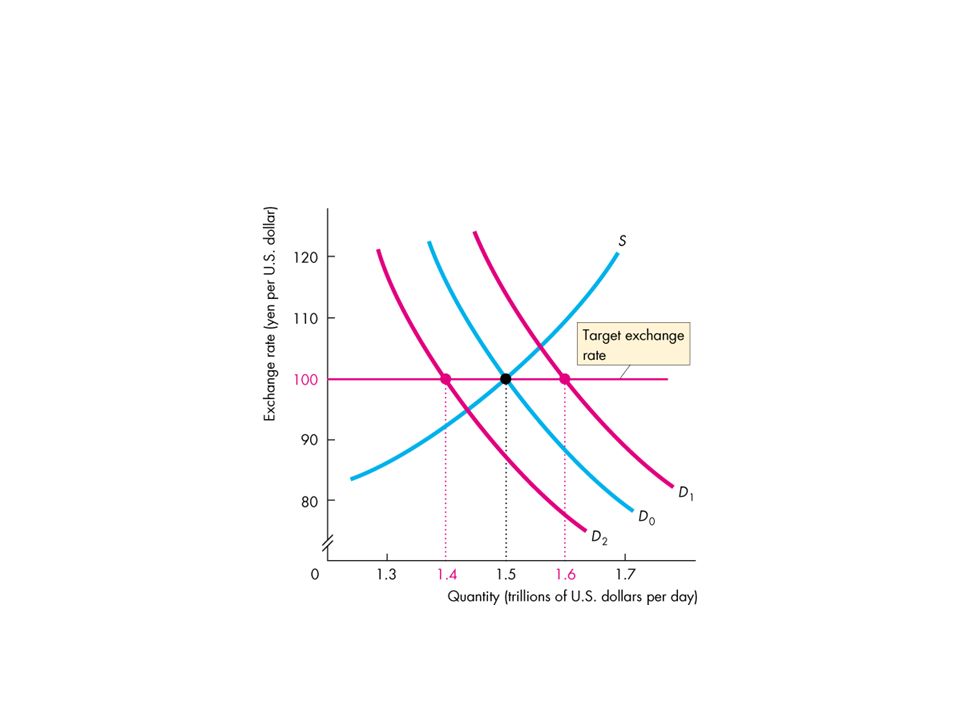

Exchange Rate Policy Three possible exchange rate policies are Flexible exchange rate Fixed exchange rate Crawling peg Flexible Exchange Rate A flexible exchange rate policy is one that permit s the exchange rate to be determined by demand and supply with no direct intervention in the forei gn exchange market by the central bank.

36

Crawling Peg A crawling peg is an exchange rate that follows a path determined by a decision of the government or the central bank and is achieve d by active intervention in the market. China is a country that operates a crawling peg. A crawling peg works like a fixed exchange rate except that the tar get value changes. The idea behind a crawling peg is to avoid wild swings in the exch ange rate that might happen if expectations became volatile and to avoid the problem of running out of reserves, which can happen w ith a fixed exchange rate.

37

외환시장개입 (Foreign Exchange Mkt Intervention) 정책은 시장환율을 왜곡시킴으로써 수출입 및 자본이동을 저해하고 상대가격 ( 인센티 브정보 ) 체계를 교란시킴 예를 들면, 중앙은행이 외환시장에 개입해 외환을 매입함으로써 원화를 시장환율보다 절하시킬 경 우 수출업자에게 보조금을 구조 수입업자 및 일반 소비자에게 세금을 인상하는 격

정책은 시장환율을 왜곡시킴으로써 수출입 및 자본이동을 저해하고 상대가격 ( 인센티 브정보 ) 체계를 교란시킴 예를 들면, 중앙은행이 외환시장에 개입해 외환을 매입함으로써 원화를 시장환율보다 절하시킬 경 우 수출업자에게 보조금을 구조 수입업자 및 일반 소비자에게 세금을 인상하는 격")

38

미국 ( 외국 ) 금리와 국내금리 금리평가식 (1+i)=(1+i*)EtSt+1/St 에서 미국금리 (i*) 를 인상할 경우 (1+i)<(1+i*)EtSt+1/St → 미국으로 자본 유출 → 자본유출을 방지하기 위하여는 국내금리 (i) 를 인상해야 하는 데 국내경제가 불경기이거나 가계 및 기업, 정부가 과다한 부채를 안 고 있다면 금리를 인상할 수 있겠는가 ? 소국개방경제 (Small Open Economy) 는 글로벌경제에서 통화정책을 독립적으로 운영하기 어렵다 (Impossible Trinity) Consider 1990 년대 말 한국을 비롯한 동아시아 위기, 2008 년 이후 미 국, 유럽 (PIGS) 들 세계경제위기

는 글로벌경제에서 통화정책을 독립적으로 운영하기 어렵다 (Impossible Trinity) Consider 1990 년대 말 한국을 비롯한 동아시아 위기, 2008 년 이후 미 국, 유럽 (PIGS) 들 세계경제위기.")

39

재정적 물가이론 (Fiscal Theory of Price Level: FTPL)- 재정정책과 통화정책의 상호작용 + = Government Debt Valuation Equation Rational agents maximize life-time expected utility subje ct to their budget (wealth, labor, and time) constraints de pendent on fiscal and monetary policies which deter mine directly and indirectly tax, govt expenditure, pri ces (interest rates, wage, foreign exchange rate, etc), and game rules (institutions, govt regulations, mkt st ructure).

- 재정정책과 통화정책의 상호작용 + = Government Debt Valuation Equation Rational agents maximize life-time expected utility subje ct to their budget (wealth, labor, and time) constraints de pendent on fiscal and monetary policies which deter mine directly and indirectly tax, govt expenditure, pri ces (interest rates, wage, foreign exchange rate, etc), and game rules (institutions, govt regulations, mkt st ructure).")

40

Arbitrage or portfolio choice among nominal assets (money balances, bonds), and real assets (investment goods) determine their relative demands or flight to quality( 안전자산 선호현상 ). Returns to real balance holdings and after-tax returns to investment goods determine the relative values of nominal and real assets. Because expectations of govt policies ultimately determine the expected returns to both nominal and real assets, monetary and fiscal policies jointly determine the price level. These mechanisms imply that the price level depends on dynamic interactions among current and expected future macro policies.

41

The price level depends fundamentally on jointly consistent combinations of current and expected future policies. Current policies directly affect prices and they indirectly affect prices through changes in expectations of future policies (Current policies may constrain future policy options, if they imply debt obligations or future expenditure commitments). These complications imply that the impacts of monetary policy(open market operations) or fiscal policy changes depend on how agents expect current and future policies to adjust to restore equilibrium.

. These complications imply that the impacts of monetary policy(open market operations) or fiscal policy changes depend on how agents expect current and future policies to adjust to restore equilibrium..")

42

Govt debt valuation equation imposes the restrictions on the inter-temporal trade-offs( 단기와 장기간의 상충관계 ) b/t current and future monetary and fiscal policies. The effects of policy changes such as a bond-financed tax cut, open-market operations, depend on current and expected future monetary and fiscal policies that are consistent with the govt budget constraint at each date. A sufficient condition for an equilibrium to exist is that the expected discounted value of real govt debt has no value at the infinite horizon; that is, a transversality (no Ponzi-game: optimal wealth accumulation of household) condition for govt debt holds at the infinite horizon.

condition for govt debt holds at the infinite horizon..")

43

References 서병한 (2014), “Interaction of Monetary and Fiscal Poli cy: Understanding of Economic Crisis, Foreign exch ange Crisis, and Policy Responses”. 서병한 (2007), “ 통화정책과 재정정책의 상호작용 : 물가안정의 재정적 조건과 중앙은행 B/S”. 2012 등

, 통화정책과 재정정책의 상호작용 : 물가안정의 재정적 조건과 중앙은행 B/S 등.")

44

Thank you for your Attention Discussion: Questions & Ansewers

Similar presentations

: 개별 가계, 기업의 의사결정, 개별시장의 균형가격 및 거래량 결정, 자원배분의 효율성 등을 다룸 거시경제학 (macroeconomics): 나라경제 전체의 고용, 생산,>")

국민대학교 노한균.>")

통화정책.>")

국민대학교 노한균.>")

>")

.>")